Each year, nearly 468 billion payment card transactions occur globally. These transactions, whether a card is swiped, scanned, or tapped, are facilitated by two essential, yet distinct, entities: the issuer and the acquirer.

These financial institutions work behind the scenes to ensure funds are available for a purchase and that money is transferred from the buyer to the seller. They also handle refunds when needed. Though the issuer and acquirer function on opposite sides of a transaction, they collaborate to keep the system running smoothly.

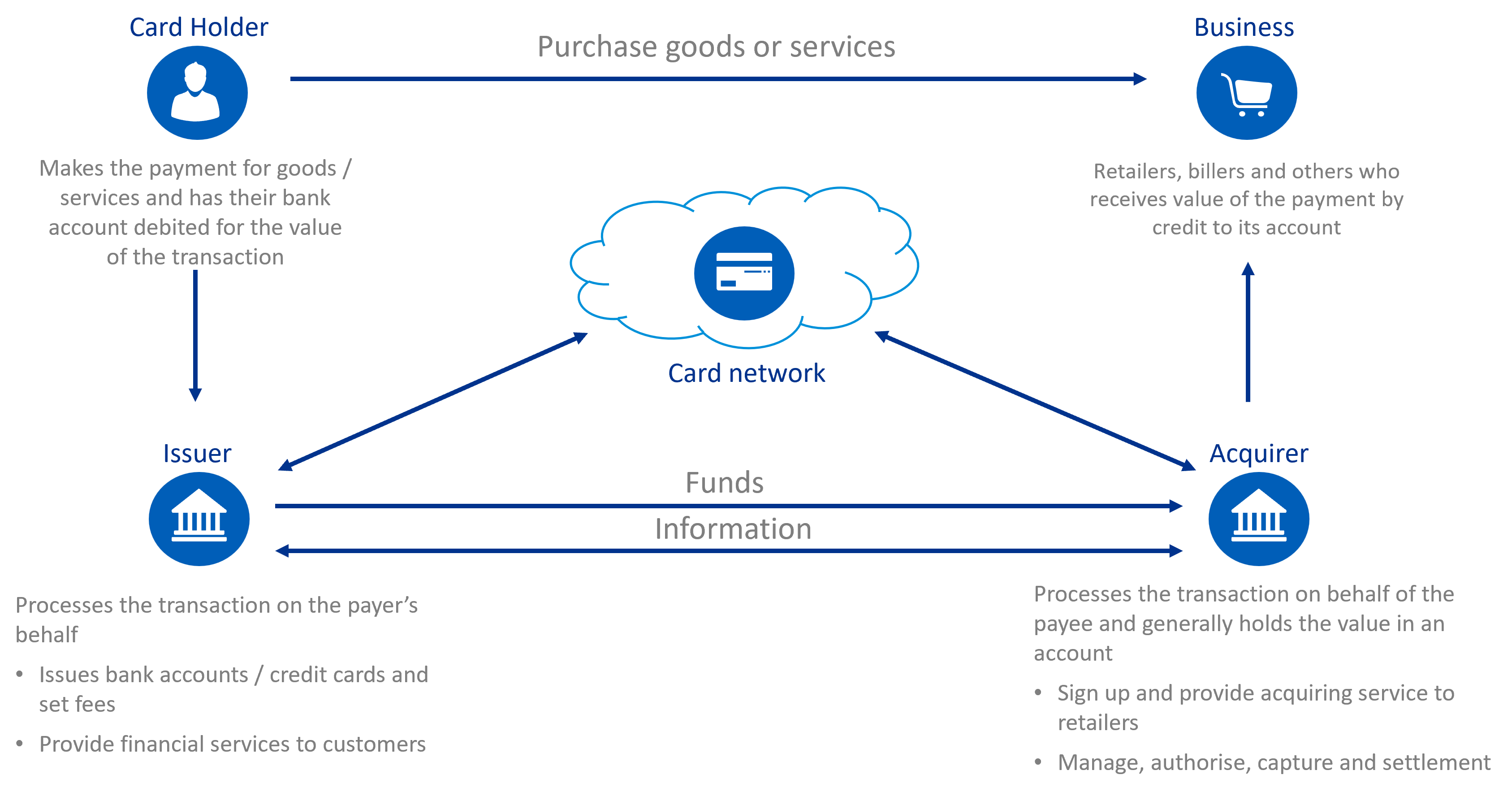

What is an Issuer?

An issuer (also known as an issuing bank or card issuer) represents the customer in a transaction. It is the financial institution that provides individuals with payment cards, such as credit or debit cards, which they use to make purchases. An issuer can be a large bank, a credit union, or any other financial organization.

In the United States, major card issuers include Chase, Bank of America, and Capital One, though smaller, regional banks and credit unions also serve as issuers.

Importantly, issuers are not the same as Visa, MasterCard, Discover, or American Express, which operate as payment networks. These networks facilitate transactions but are not involved in individual transactions themselves. Issuers and acquirers manage the processing of these payments.

When issuing credit, the issuer evaluates a customer’s creditworthiness by reviewing factors such as credit score and financial history. Once approved, the cardholder is granted access to a line of credit, which essentially functions as a loan that the issuer is responsible for managing.

If the cardholder fails to repay the loan on time, the issuer is liable for the debt. Furthermore, issuers are responsible for handling chargebacks – instances where a customer disputes a transaction and requests a refund. While the issuer helps review these requests, its decision can be challenged, but it plays a pivotal role in determining whether or not a chargeback is valid.

What is an Acquirer?

If the issuer represents the customer, the acquirer (or acquiring bank) represents the business. Acquirers are financial institutions that equip businesses with the tools they need to accept payments from issuers. They are responsible for obtaining the funds from the issuer and depositing them into the merchant’s account to complete the transaction.

Acquirers also provide businesses with a unique merchant ID that enables them to communicate with card networks to facilitate transactions. In some cases, acquirers also act as payment processors, but more often, they function as intermediaries, ensuring that a transaction reaches the appropriate card network and is processed correctly.

While acquirers can be members of various card networks and partner with several card processors, they ensure that money provided by the issuer is funneled into the business’s account.

Acquirers also carry certain financial risks. They are obligated to adhere to stringent security measures set by the Payment Card Industry Data Security Standards (PCI DSS). Failing to comply with these standards can lead to increased liability, particularly in the case of data breaches or fraudulent transactions.

If a chargeback occurs, the acquirer is responsible for repaying the issuer, which then returns the funds to the customer. This process can incur significant costs for the acquirer, especially if the business involved is unable to pay its debts. To mitigate this risk, acquirers may require businesses to go through a risk assessment process and maintain reserve funds or lines of credit to cover such costs.

What’s the Difference Between an Acquirer and an Issuer?

The issuer is responsible for maintaining the credit or debit accounts of cardholders, offering them access to either their funds or a line of credit. On the other hand, the acquirer handles the transaction by ensuring the funds are transferred to the merchant’s account and maintains records of the payment.

Here’s how the two institutions collaborate in a typical transaction:

- The customer begins the payment by swiping, tapping, or scanning their card at a point-of-sale (POS) terminal.

- The business’s payment processor sends the transaction information to the acquirer, which then submits it to the card networks.

- The card networks check with the issuer to confirm whether the customer has sufficient funds or credit. The issuer approves or declines the transaction based on the cardholder’s account.

- The response is sent back through the card network to the acquirer, who informs the business about the transaction’s status.

- If the transaction is approved, funds move from the issuer to the acquirer, who deposits them into the merchant’s account.

Even for recurring transactions, like subscription payments, the issuer and acquirer continue to communicate to process payments on an ongoing basis. Payment platforms like Stripe manage these transactions, ensuring smooth processing.

In the case of a chargeback, the roles of the acquirer and issuer are reversed:

- The cardholder requests a chargeback from the issuer, providing evidence for the reversal.

- The issuer assesses the request and decides whether to approve or decline the chargeback.

- If approved, the issuer communicates with the acquirer to return the funds to the customer.

- The acquirer processes the chargeback, and the business is responsible for covering the cost.

In essence, while the issuer represents the customer and the acquirer represents the business, both work in tandem to ensure payments are completed and disputes are resolved.