🔐 What Is a “Payment Stablecoin”?

Under the GENIUS Act, a payment Stablecoin is defined as a digital asset that:

-

Is used—or intended—for payment or settlement.

-

Is redeemable for a fixed amount of fiat.

-

Creates a reasonable expectation of maintaining stable value.

Important exclusions: fiat currency, bank deposits (including tokenized ones), and securities.

🏛️ Key Provisions of the GENIUS Act

-

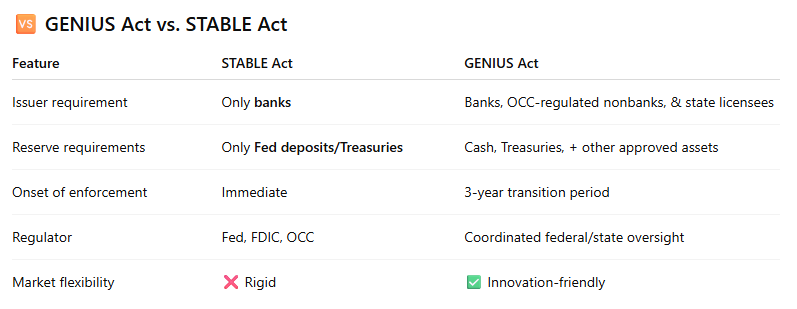

Permitted Issuers Only

Only licensed entities—such as subsidiaries of insured banks, OCC-approved nonbanks, or state-regulated issuers—can issue Stablecoins. -

Full 1:1 Reserve Backing

Issuers must maintain liquid reserves (cash, Treasuries, etc.) equal to outstanding tokens. Monthly reserve disclosures are mandatory. -

Strict AML & BSA Compliance

Issuers must adhere to anti-money laundering (AML), Bank Secrecy Act (BSA), sanctions rules, and support seizure/cold wallets for legal orders. -

Bankruptcy Priority for Holders

Stablecoin users get priority claims on reserve assets over other creditors—raising potential cost concerns for traditional banks. -

Digital Asset Service Provider (DASP) Rules

After three years, any platform offering Stablecoins must ensure they’re issued by an approved entity. Foreign issuers can still enter the U.S. market if they adhere to comparable supervision and U.S. reserve requirements. -

Federal & State Regulator Coordination

Issuers under $10 billion can operate under state licensing, but must convert to federal supervision once meeting that issuance threshold

📈 Why the GENIUS Act Matters

-

Historic Milestone: This is the first major federal Stablecoin legislation to pass in U.S. Congress.

-

Industry-Friendly: Designed to foster innovation while ensuring consumer protection and financial stability.

-

Macro Impact: With the 1:1 backing rule, Stablecoin issuers may significantly boost demand for U.S. Treasury bills—possibly in the $1 trillion range.

-

Institutional Entry: The bill clears the path for companies like Walmart, Amazon, and major banks to issue branded Stablecoins.

⚠️ Overlooked Risks & Criticisms

-

Bank Exposure: Bankruptcy-priority rules may financially burden banks issuing or holding Stablecoin reserves.

-

Regulatory Gaps: House amendments (or lack thereof) may leave room for weaker oversight.

-

Foreign Issuer Compliance: Non-U.S. issuers must meet stringent comparability and registration standards—a potential entry barrier.

-

House Vote in “Crypto Week”: House leadership has scheduled the floor vote this July, bypassing merging with the STABLE Act—expect a clean pass.

-

Presidential Approval: If House passes it, the bill heads to President Trump’s desk—where he’s signaled strong support .

-

Transition & Enforcement: A 3‑year compliance window follows—after which unapproved Stablecoins may be restricted from U.S. services.

🧩 Final Take

The GENIUS Act is a pivotal step in legitimizing Stablecoins in America—as usable money, not speculative tokens. Its balanced framework combines reserve backing, AML compliance, and stable-holder protection with a scalable licensing model suited to both established financial institutions and innovative fintech players.

Once enacted, it promises to reshape the payments landscape—empowering crypto-native firms, retail giants, and banks alike to integrate U.S.-backed Stablecoins into everyday commerce. But for developers, issuers, and platforms, implementation will hinge on carefully navigating licensing, compliance, and evolving regulatory expectations.