The UK banking system offers a variety of payment schemes to suit different transaction types—domestic or international, urgent or routine, low-cost or high-value. Whether you’re a business owner, employee, or consumer, understanding these schemes helps you choose the most efficient, cost-effective way to move your money.

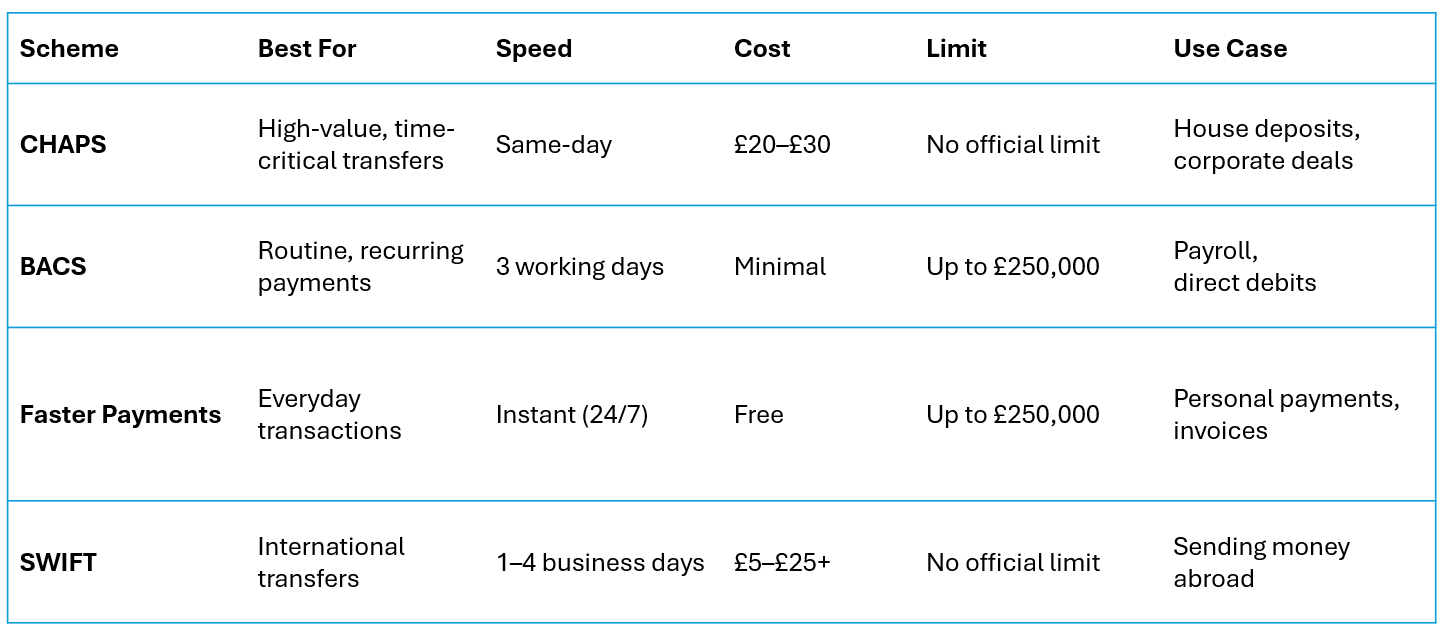

1. CHAPS (Clearing House Automated Payment System)

Purpose: High-value, time-sensitive domestic transactions

Processing Time: Same day (typically within hours)

Cost: £20–£30 (varies by bank)

Transfer Limit: No official minimum or maximum, but often used for amounts over £10,000

Best for: Large, urgent payments like house deposits or corporate transfers

CHAPS is ideal when you need to send a large amount of money quickly and securely. Payments are processed in real time and are typically received on the same business day. However, banks often have strict cut-off times (typically before 6 pm) and charge a fee for each transaction.

How to use CHAPS:

-

Available online, by phone (for some customers), or at your bank branch.

-

You’ll need the payee’s name, account number, sort code, and reference.

Pros:

-

Real-time processing

-

Ideal for large, time-sensitive transactions

-

Reliable and secure

Cons:

-

High transaction fees

-

Irrevocable once sent

-

Cut-off times vary between banks

2. BACS (Bankers Automated Clearing Services)

Purpose: Routine domestic payments such as payroll, supplier payments, and direct debits

Processing Time: Up to 3 working days

Cost: Usually free or minimal

Transfer Limit: Varies by bank, can go up to £250,000

Best for: Payroll, subscriptions, and other recurring payments

BACS handles two types of transactions:

-

Direct Debit: The recipient pulls funds from your account (with authorization).

-

Direct Credit: You push funds to a recipient’s account.

BACS is highly secure and widely used for regular, non-urgent payments. It’s cost-effective and paperless, making it suitable for businesses.

How to use BACS:

-

Requires the recipient’s sort code and account number.

-

Payments can be made through a bureau or directly via your bank’s platform.

Pros:

-

Secure with SSL encryption (Bacstel-IP)

-

Cost-effective for regular and bulk payments

-

Supports automation with accounting software

Cons:

-

Takes up to 3 days to clear

-

Limited to business working days

-

Subject to strict cut-off times

3. Faster Payments System (FPS)

Purpose: Instant domestic transactions

Processing Time: Usually within seconds, 24/7

Cost: Usually free

Transfer Limit: Up to £250,000 (varies by bank)

Best for: Small to medium everyday payments

Launched in 2008, Faster Payments are commonly used for quick transfers between UK bank accounts. Whether you’re sending money to friends or paying a supplier, this scheme ensures near-instant processing.

Types of Faster Payments:

-

Single Immediate Payments: One-off payments made online, by phone, or in branch

-

Standing Orders: Regular, scheduled payments

-

Forward-Dated Payments: Payments set for a future date

-

Direct Corporate Access: Bulk payments submitted by businesses

How it works:

-

Enter recipient’s sort code and account number.

-

Your bank verifies the funds and identity before processing.

Pros:

-

Real-time transfers 24/7

-

Convenient via online, phone, or mobile banking

-

Ideal for recurring and personal transactions

Cons:

-

Some banks may impose limits on transaction amounts

-

Mistakes can be difficult to reverse

-

May require investment for businesses to integrate

4. SWIFT (Society for Worldwide Interbank Financial Telecommunication)

Purpose: Secure international money transfers

Processing Time: 1–4 business days

Cost: £5–£25+, plus potential intermediary bank fees

Transfer Limit: No official limit (subject to available funds and fees)

Best for: International payments between bank accounts

SWIFT is a global messaging network that connects banks across borders. It enables businesses and individuals to send money securely around the world. The system routes payment instructions through a chain of correspondent banks, which can add to the time and cost.

Information required:

-

Recipient’s name and address

-

Bank name and address

-

SWIFT/BIC code

-

Account number or IBAN

Transfer speeds:

-

Standard (D+2): Two business days

-

Urgent (D+1): One business day

-

Express (D+0): Same-day delivery

Pros:

-

Secure and transparent

-

Trackable with detailed information

-

Widely accepted for international business

Cons:

-

Slower than domestic options

-

Can be expensive due to intermediary fees

-

Exchange rates may vary

The Future of UK Payments

The UK payments landscape is constantly evolving with digital banking and innovations like Open Banking. A major upcoming development is the New Payments Architecture (NPA), which will eventually replace traditional systems like BACS, CHAPS, and Faster Payments with a unified, modernized infrastructure.

Summary Comparison

Understanding these payment options empowers you to make informed financial decisions—whether you’re paying a supplier, managing payroll, or sending money overseas. Choose the one that fits your transaction type, urgency, and cost expectations.