The Need for Efficient Cross-Border Payments

In today’s interconnected economy, the demand for seamless, cost-effective, and speedy international payments is higher than ever. While traditional banking networks have long facilitated these transactions, the emergence of Stablecoins introduces a compelling alternative that could redefine financial transfers worldwide.

Traditional Banking: The Role of BIC and SWIFT Codes

BIC (Bank Identifier Code) and SWIFT (Society for Worldwide Interbank Financial Telecommunication) codes are unique identifiers assigned to financial institutions, ensuring the secure and accurate routing of international wire transfers through the SWIFT network.

How BIC/SWIFT Codes Work:

Initiating the Transfer: The sender’s bank submits a request containing the recipient’s banking details, including their SWIFT code.

Routing and Processing: The SWIFT network transmits the message, directing the funds through intermediary banks as necessary.

Final Settlement: The recipient’s bank verifies the transaction and deposits the funds into the designated account.

Limitations of Traditional Systems:

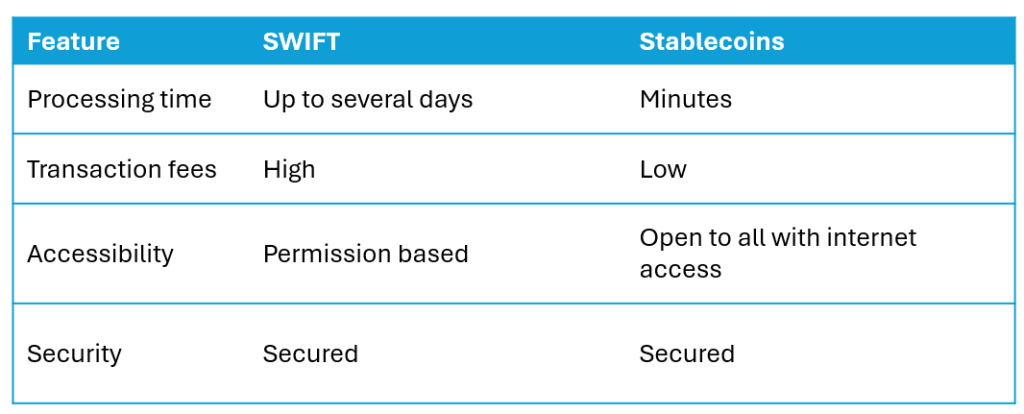

Slow Processing Times: Transactions may take several days to settle due to intermediary banks and varying time zones.

High Costs: International wire transfers often incur significant fees.

Limited Accessibility: Many individuals and businesses, particularly in underbanked regions, lack access to traditional banking services.

Stablecoins: A Revolutionary Alternative

Stablecoins are blockchain-based digital currencies designed to maintain a stable value by being pegged to traditional assets such as fiat currencies or commodities. They offer a novel approach to global transactions, providing several advantages over conventional wire transfers.

How Stablecoin Transactions Work:

Transaction Initiation: The sender transfers Stablecoins from their digital wallet to the recipient.

Blockchain Processing: The transaction is verified and recorded on a decentralized ledger, ensuring security and transparency.

Instant Settlement: Funds become available to the recipient almost immediately.

Key Advantages of Stablecoins:

Speed: Transactions clear in minutes, regardless of geographic location.

Cost Efficiency: Fees are significantly lower than those associated with traditional bank transfers.

Accessibility: Anyone with internet access can use Stablecoins without requiring a bank account.

The Impact on Traditional Banking

The rise of cryptocurrencies and stablecoins is forcing financial institutions to adapt. Some key implications include:

-

Disintermediation: Stablecoins enable direct, peer-to-peer transactions, reducing reliance on traditional banks as intermediaries.

-

Innovation Pressure: Banks must modernize their services to compete with the efficiency and cost-effectiveness of digital currencies.

Challenges Facing Stablecoins

Despite their potential, stablecoins and other digital assets face hurdles that could affect their adoption:

-

Regulatory Uncertainty: Governments and financial regulators are still developing clear guidelines for stablecoin usage.

-

Market Volatility: While stablecoins aim for price stability, broader cryptocurrency markets remain volatile.

-

Awareness and Adoption: A lack of education and familiarity with blockchain technology can hinder widespread adoption.

Emerging Solutions: Alternative Payment Platforms

As financial systems evolve, multiple platforms are emerging as alternative solutions to traditional banking. Examples include:

-

Ripple (XRP): Utilizes blockchain technology to enable near-instant cross-border payments with low transaction fees, collaborating with banks and financial institutions.

-

Stellar (XLM): Provides a decentralized network designed for fast and low-cost international transactions, focusing on financial inclusion.

-

Circle (USDC): A widely adopted Stablecoin that supports cross-border transactions with transparency and regulatory compliance.

-

Airwallex: A fintech platform offering cross-border payments, multi-currency wallets, and global financial solutions tailored for businesses.

-

Wise (formerly TransferWise): A cost-efficient platform for international payments using real exchange rates to reduce fees.

-

Payoneer: A global payment platform enabling businesses and freelancers to receive and send payments internationally with lower costs.

-

Revolut: A digital banking solution offering international payments, multi-currency accounts, and competitive foreign exchange rates.

Implications for Global Transactions:

-

Competitive Alternatives: Businesses can leverage multiple payment platforms for cost-effective international transactions.

-

Financial Innovation: The emergence of these platforms highlights the rapid advancements in financial technology.

Expert Insights and Industry Predictions

Leading financial organizations have weighed in on the impact of cryptocurrencies and Stablecoins:

-

World Economic Forum: Estimates suggest that by 2027, 10% of global GDP could be held in digital currencies.

-

International Monetary Fund (IMF): Research indicates that Stablecoins could provide a more efficient solution for cross-border payments, especially for low-value transactions.

Conclusion

The financial landscape is undergoing a profound transformation, with Stablecoins emerging as a viable alternative to traditional banking mechanisms. While BIC and SWIFT codes remain integral to global finance, the advantages offered by Stablecoins—speed, affordability, and accessibility—are hard to ignore. As regulations evolve and adoption grows, Stablecoins are poised to play an increasingly significant role in the future of global payments.