Understanding Interchange Fees

Interchange fees are the charges merchants incur when processing card payments from customers, whether online or in-store. These fees are not a flat amount per transaction but instead involve multiple parties:

- The card issuer: This is the bank or financial institution that issued the customer’s card.

- The card network: Examples include Visa, Mastercard, Discover, and American Express.

- The acquirer: This is the merchant’s bank or payment processor.

These fees are influenced by a variety of factors, including the type of card used, the country where the card was issued, and whether the payment was made online or in person. Understanding how interchange fees work and the pricing models that affect them is crucial for businesses looking to minimize costs.

How Interchange Fees Work

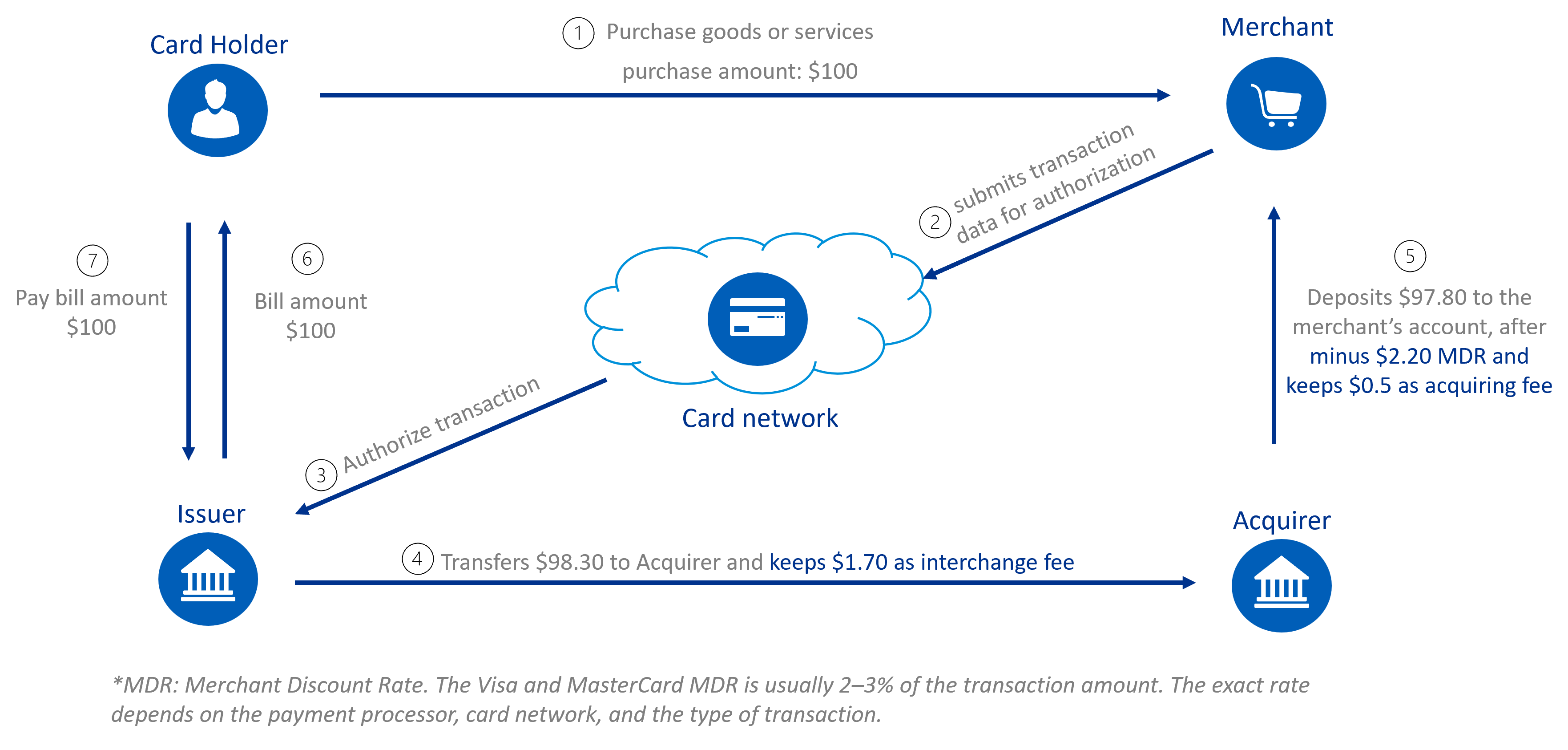

Let’s walk through the typical process of an in-store card payment:

During this process, the acquirer pays interchange fees to both the card issuer and the card network. These fees are then passed on to the merchant, typically with an added markup to cover handling costs.

A significant portion of these fees compensates the card issuer for the credit risk and potential fraud, while the rest goes to the card network. Typically, interchange fees are a combination of a percentage of the transaction value and a fixed fee.

How Much Are Interchange Fees?

The amount merchants pay in interchange fees can vary widely depending on multiple factors. Generally, merchants can expect to pay between 2-3% of the transaction value, plus a fixed fee (usually around $0.20). For example, if a customer makes a $150 purchase at a store, and the interchange fee rate is 1.5%, the merchant would pay $2.25. From this, the acquiring bank might receive $0.30, the card network $0.20, and the card issuer $1.75. The merchant would keep the remaining $147.75 from the sale. These fees are generally not visible to the customer, as they’re built into the pricing.

Factors That Influence Interchange Fees

Several factors determine the interchange fees a business will face:

-

Card-present vs. Card-not-present Transactions In-person payments (card-present) usually come with lower fees than online or phone transactions (card-not-present), as the latter carry a higher risk of fraud.

-

Merchant Category Code (MCC) Each business is assigned an MCC based on its industry, and this can affect the interchange fees. High-risk industries like airlines usually face higher fees compared to lower-risk businesses like charities.

-

Card Network Fees differ between card networks. For instance, Visa and Mastercard typically have lower fees than American Express, which often has higher costs due to different business models.

-

Credit vs. Debit Cards Credit card transactions typically carry higher fees than debit card payments because they involve more risk. Credit card issuers use interchange fees to offset the cost of offering credit and rewards programs.

-

Place of Issuance Cross-border transactions tend to have higher fees due to the complexities of international payments, including currency conversion and added security.

-

Security Measures Merchants that implement enhanced security measures, such as tokenization or requiring card security codes, might benefit from lower fees, as these practices reduce the risk of fraud.

-

Consumer vs. Commercial Cards Commercial or business cards generally have higher interchange fees than personal consumer cards due to the higher associated costs.

-

Regional Differences Different regions have various regulations. For example, in the European Union, interchange fees are capped at 0.3% for credit cards and 0.2% for debit cards, whereas in the U.S., these rates are not capped.

Interchange Fee Pricing Models

Payment processors use different pricing models to calculate how interchange fees are charged. Here are the most common types:

-

Interchange Plus Pricing (Interchange++ or called IC++) This model is the most transparent, as businesses can see exactly how much they’re being charged by the card issuer, network, and acquirer for each transaction.

-

Tiered Pricing In this model, transactions are grouped into tiers based on the type of card used or risk factors. It can be more difficult for businesses to predict costs, as fees vary based on these tiers.

-

Flat-rate Pricing (Blended Pricing) This model charges a fixed rate per transaction, regardless of card type or other variables. It simplifies budgeting for businesses, though it might not always be the most cost-effective depending on the type of transactions.

-

Subscription Model With a subscription model, businesses pay a fixed monthly fee in exchange for lower per-transaction costs. This can be beneficial for high-volume businesses but requires careful consideration.

Impact of Interchange Fees on Your Business

Interchange fees can significantly impact your business in several ways:

- Operating Costs: For businesses with high transaction volumes, these fees can make up a substantial portion of operating expenses.

- Pricing Strategy: Some businesses may need to adjust prices to cover interchange fees, which can affect customer satisfaction.

- Cash Flow: Since interchange fees are deducted before funds are deposited into the business’s account, managing cash flow becomes more complex.

- Payment Preferences: Businesses may encourage customers to use lower-cost payment methods, such as debit cards or cash.

- Payment Processor Selection: The choice of payment processor can significantly affect the interchange fees you pay, so it’s important to find a cost-effective solution.

For businesses that operate internationally, it’s also essential to be aware of foreign exchange fees, which can add another layer of cost to cross-border transactions.

Tips for Reducing Interchange Fees

Reducing interchange fees can be challenging, as the card networks determine the rates, which fluctuate based on several factors. However, businesses can adopt several strategies to help lower these costs:

-

Negotiate with Your Processor: If your business handles a large volume of transactions, you may have the opportunity to negotiate better rates with your payment processor.

-

Choose the Right Payment Processor: Different payment processors offer varying pricing models. By selecting a processor whose model aligns better with your transaction volume and patterns, you may be able to lower your fees.

-

Enhance Card Processing Practices: Following best practices for card processing can help businesses qualify for lower interchange fees. Key actions include:

- Settling Transactions Quickly: Settle transactions promptly, ideally within 24 hours, to avoid higher processing costs.

- Securing Card Data: Implementing advanced security measures, such as point-to-point encryption and tokenization, can help reduce interchange fees.

- Submitting Complete Transaction Data: For certain card types, such as corporate or government cards, providing additional transaction information (Level 2 and Level 3 data) can lead to lower interchange rates.

-

Promote Debit or Cash Payments: Debit card transactions usually carry lower interchange fees than credit cards, and cash transactions don’t have any interchange costs. Encouraging customers to use these payment methods can help reduce overall fees.

-

Add a Surcharge or Service Fee: In certain regions, businesses may be allowed to impose a surcharge or service fee on credit card transactions to offset interchange fees. However, this practice is regulated and may not be allowed everywhere or for all card types, and it may not be well-received by customers.

-

Review Processing Statements Regularly: Interchange fees are subject to change, often twice a year. It’s important to regularly check your processing statements to stay informed about any fee adjustments and fully understand the charges you’re facing.

By understanding and strategically managing interchange fees, businesses can reduce costs and improve profitability.